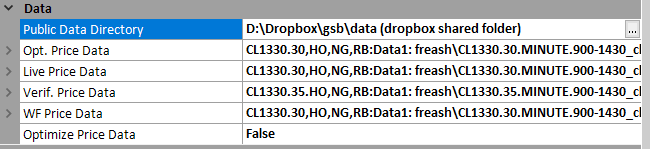

Data

To keep is really simple, you could chose OPT price data as ES.30 minute, and all other fields blank. This however fails to use a lot of the power of GSB to get better out of sample results. For more details read on. 2021 March update. These features are now rarely used due to more robust system building techniques.

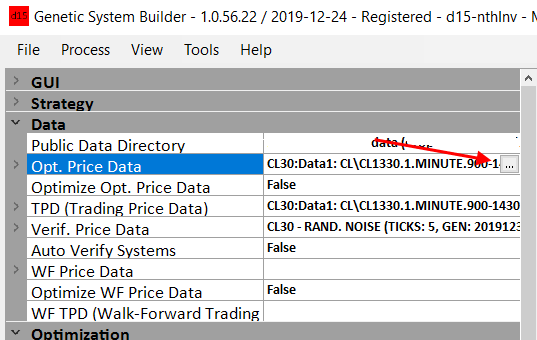

Opt Price Data

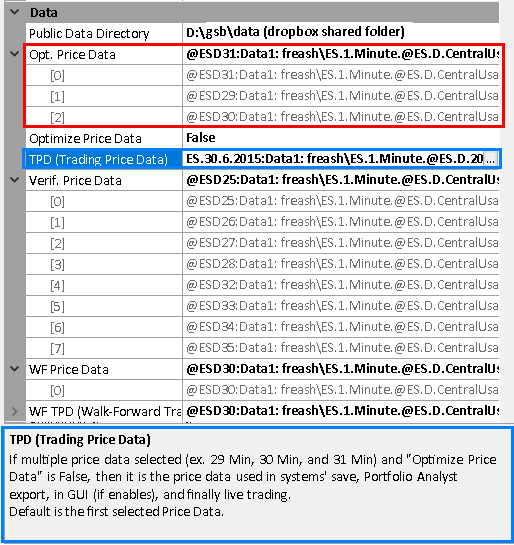

This is what GSB builds systems on. Using multiple time frames results in much more robust systems. It would be ok to use a single time frame, but verify on multiple time frames. i.e. build on 30 minute, but verify in 29,31 Even better would be to verify on 25,26,27,28,29,31,32,33,34,35.

Most often I build on 29,30,31 minute bars and verify on 25,26,27,28,29,31,32,33,34,35 minute bars. GSB will be slower building on 29,30,31 minute bars than 30 minute bars, and use more ram.

Note in the example below, 29 minute bars are made from 1 minute bars, times 29.

In this example gold is used as data2.

For example 5 minute bars could be used * 6 to make 30 minute bars.

Opt price Data True / False

Default is false. If False GSB will build systems on all data streams using the same parameters. If true is used GSB will build systems on only one time frame, but genetically chose the best time frame. Its likely some systems could be on each time frame, but the best time frame is more likely to be genetically chosen more often.

TPD (Trading price data)

You may build systems on 29,30,31 minutes, but you only trade the 30 minute. If this is the case chose 30 minute. Default if blank is the first selected price data.

Verification Price Data.

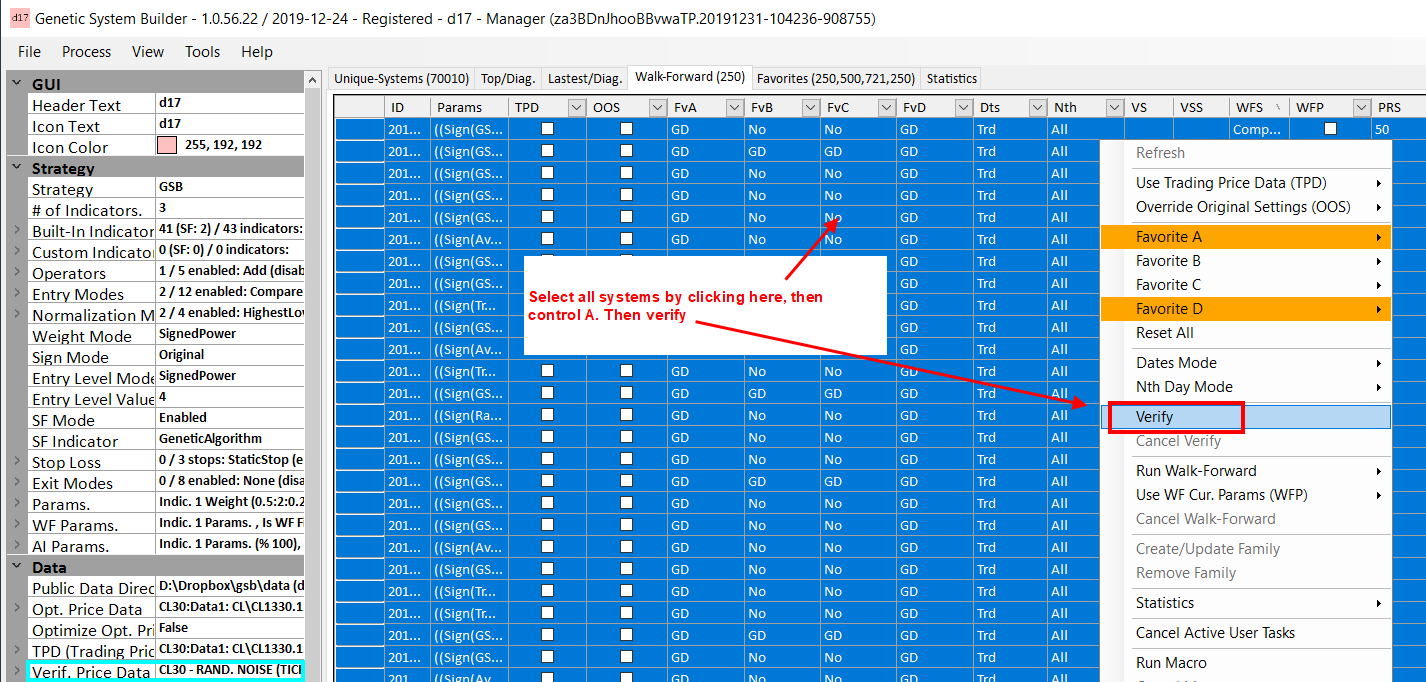

A system can be verified on other time frames or markets to test how valid the system is. Right click a system and click verify. For Crude oil you can verify on heating oil and unleaded gas. S&P 500 can be verified on Mid Cap 400, Nasdaq, Dow & Russell 2000.

Verify Price Data

This data is used in Verification. To add Verify Data/Filter you need to add the data same way you load the Price data.

See this link for more details.

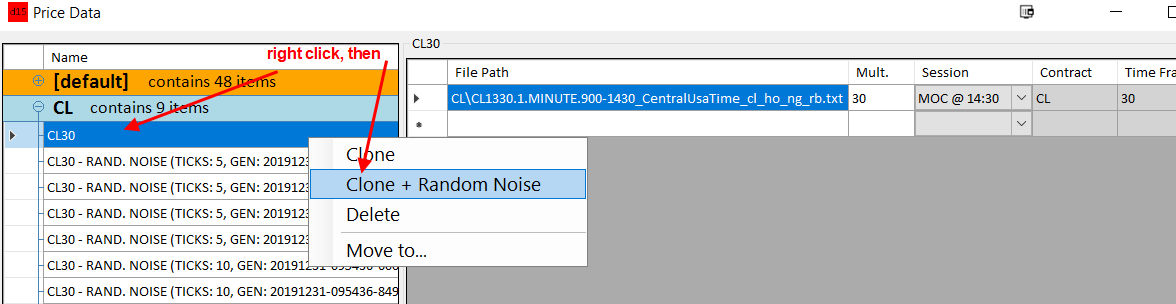

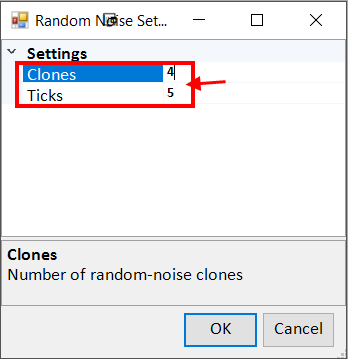

You can also add random noise to the verification data. It is recommended to add 4 data streams of 4 ticks random data, and 4 data streams of 8 ticks random data.

Follow the steps below to do this.

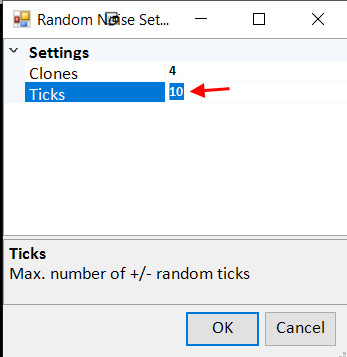

Change clones to 4, and ticks to 5. Repeat the process with ticks 10

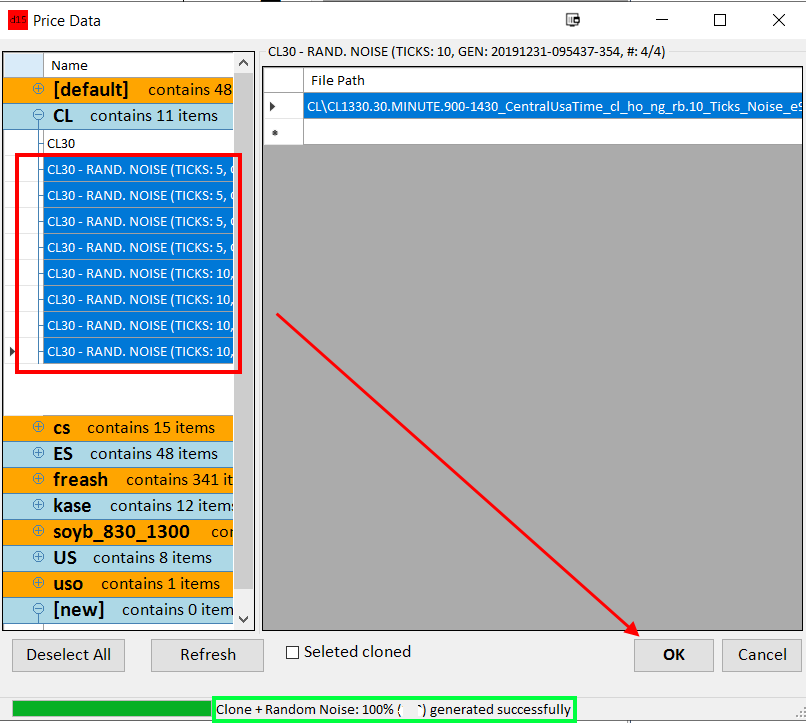

It may take a minute to make the random data.

Once its done, select the data and click OK.

The logic is, if a system passes verification with random noise on the data, and or using multiple time frames, it is much more robust and likely to work out of sample. For a 30 minute system, verification of all bars from 25 to 35 minutes is a good test. A important setting is under performance filter, verification. The default is profit factor of 1.8, and pearsons of 0.85. You may choose to adjust these settings a little if needed. If to few systems verify, reduce these values. If you have to many systems, increasing pearsons to 0.95 will help.

Note: your charts on TS must be on local time to have more than one data stream. If your computer isn't on Central USA time zone, to add more data streams they must all be on the same time zone. (Including data1) If you get this wrong, then data streams may be looking into the future and delayed. All results will be invalid.

If you have say 330 minutes in a day, and you have 30 minute bars, there are 11 bars in a day. If you then use 29 minutes, this makes 12 bars in a day. 31 minutes makes 10 bars in a day. These differing bar intervals stress test the GSB oscillators, reducing the tendency to over curve fit. If you choose other intervals, its is recommend that you get a different number of bars above and below the central time frame. For more detail on the significant implications of this, look at the market validation videos. https://trademaid.info/video.htm This is a very important video.

Note a trading systems verification can use one or both of two methods. You verify by VSS or VS.

WF Price Data.

You can walk forward on 29,30,31 min bars, or 30 minute bars. What is best has not yet been determined.

WF (TPD)

If you walk forward on multiple time frames, chose the central one for WF (TPD) If multiple markets use the primary one.

Description box. (In blue here)

This describe each feature you have your mouse on.

Supplying Data to GSB

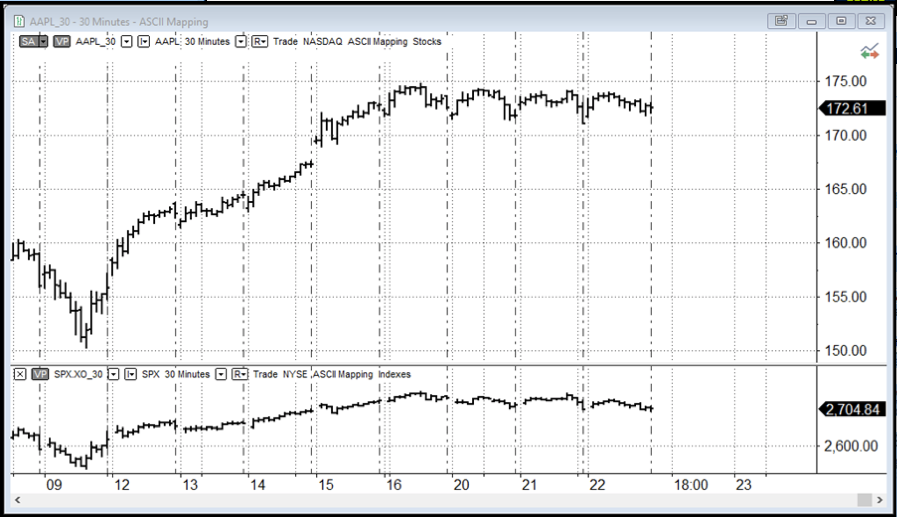

We are planning to develop a trading system in GSB using AAPL as Data 1 and SPX as Data 2 or in GSB terms as Primary and Secondary Data.

We have set up a chart of Apple (AAPL_30) with the S&P500 index SPX.XO_30 as Data 2 as shown in FIG 1.31. To add SPX as Data 2 click Insert – Instrument and select SPX.XO_30.

Please note that it has been found that GSB uses secondary data preferably an index in the case of stock systems because this has been shown to develop superior trading systems. One possible issue is compatibility between the session times for primary and secondary data. You will need to make sure that the times are matching. Sessions times can be modified under Instruments – Edit Instruments.

FIG 1.31 Chart AAPL & SPX.30

FIG 1.31 Chart AAPL & SPX.30

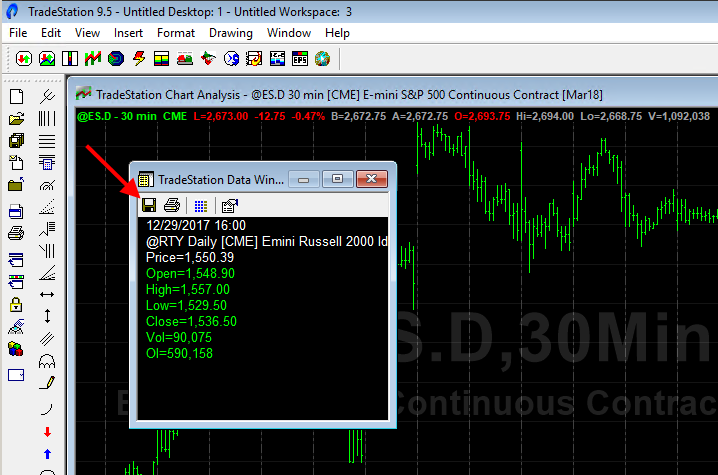

Export data from MultiCharts/Trade Station to GSB and then locate the correct GSB location which is:

Local Disk (C) GSB – GSB (Manager) – Data - PriceData

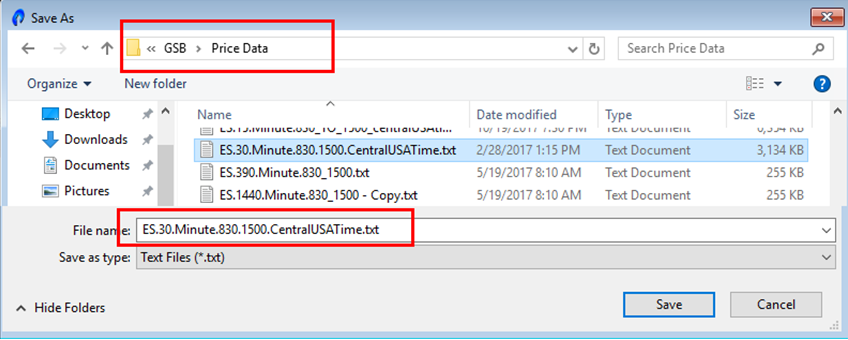

GSB requires files names in a set format so we now need to modify the file name to

Supported file format:

Filename formats that can be used are

symbol.15.minutes.SessionTime.Anthingyoulike.txt IE ES.15.minutes.830_1500CTusa.txt

symbol.10.seconds.SessionTime.Anthingyoulike.txt IE ES.10.seconds.830_1500CTusa.txt

symbol.10.Kase.1 tick.SessionTime.Anthingyoulike.txt

symbol.10.Range.1 tick.SessionTime.Anthingyoulike.txt

symbol.150.Tick.1 tick.SessionTime.Anthingyoulike.txt

symbol.150.heikinashi.SessionTime.Anthingyoulike.txt

symbol.150.ha.SessionTime.Anthingyoulike.txt

If you want to use daily bars, then use this format.

ie 830 to 1500 in minutes bars = 6.5 * 60 = 390 minutes.

symbol.390.minutes.SessionTime.Anthingyoulike.txt

See this note on Renko & Point Orignal bars.

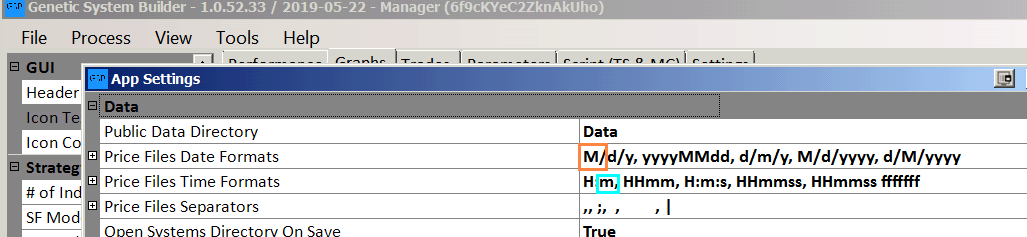

GSB should auto detect date, time formats, but you need to get the file name correct.

If not add the correct settings in app-settings data.

Note that M is month, and m is minute.

For more details see https://docs.microsoft.com/en-us/dotnet/standard/base-types/custom-date-and-time-format-strings

Note we are using central USA data time zone local time 830 to 1500 time, not 830 to 1515 time. You can't mix time zones, so if you are on another time zone, and want to add other data streams mixed with ES etc, use only data from your own computer.